Over the last several weeks, investors faced the realizations that the Fed might take one more step on the road to normalization and that Mario Draghi’s ‘Do what it takes’ might have morphed into ‘if pushed, we could do a bit more.’ This predictably brought a jump in bond yields around the world and talk of taper tantrum, the sequel. The more excitable of the monetary policy hawks and doves both tend to hear the words taper tantrum with a sense of horror. To many doves, the jump in yields following Bernanke’s taper talk threatened a 1937-like disaster and was proof that even a small step toward normalization is fraught with danger. To many hawks, the incident shocked the skittish Fed, causing it to hold rates unnaturally low ever since.

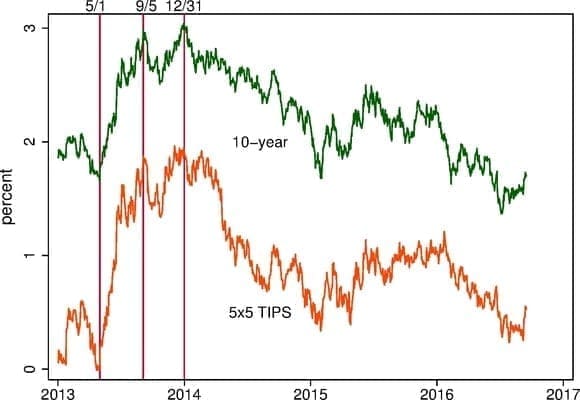

We think the tantrum period does hold important lessons for today, but those hawk and dove stories just given don’t make sense. Financial data make the taper period appear as if market participants perceived the dawning of a golden age—stock market soars, risk spreads shrink, and indicators of future real yields bounce back from the gloomiest values ever recorded. If warranted, such rosy views should have been welcome. But in the years since the end of the tantrum, those nominal and real yields have slowly slid back to the gloomy pre-tantrum levels (Fig. 1). The simplest story to tell of the full period is one of (ex post, at least) unwarranted optimism that was quickly gained and slowly dissipated. That perspective offers up some important lessons for today’s policy environment.

Fig. 1. The 10-year Treasury yield and 5-year forward 5-year (real) TIPS yield. Sources: FRED and Bloomberg.

Let’s review some tantrum facts. Over the 4 months between the beginning of May 2013, just before Bernanke first spoke of the taper, and the beginning of September, the Treasury 10-year yield jumped nearly 150 basis points (Table 1). A hawkish jolt? Perhaps, but measures of the expected path of the policy interest rates didn’t shift much.[1] Moreover, over those four months, the S&P500 rose almost 4 percent and various risk spreads fell. One of our favorite indicators, the 5-year forward, 5-year real yield on TIPS (labeled 5×5 TIPS) had sagged to zero over the beginning of 2013. Over the tantrum months, this indicator of real yields coming 5 to 10 years in the future rebounded by almost 200 basis points, rising to a level not seen since mid-2011.

| 2013 | 2016 | |||

| Yield (%) | 5/2 | 9/5 | 12/31 | 9/1 |

| 10-year Treas. | 1.66 | 2.98 | 3.04 | 1.57 |

| Baa spread | 2.81 | 2.55 | 2.33 | 2.62 |

| 5×5 TIPS | 0.04 | 1.88 | 1.95 | 0.30 |

| S&P500 | — | 3.60 | 15.70 | 35.88 |

Table 1. Yields on three dates around the tantrum and recently. 10-year Treas. is the Treasury 10-year constant maturity yield; Baa spread is Moody’s Baa index minus 10-year Treas.; 5×5 Tips is the 5-year forward 5-year TIPS (real) yield; S&P500 is the percent change in the S&P500 from 5/2/2013 to the date for the column. Sources: FRED except for 5×5 Tips which is from Bloomberg.

One of us (Faust) was at the Fed at the time and worked on analysis pointing out that much good had come with the bad. The 10-year nominal yield and mortgage rates were up, which would hurt housing, but the net effect of all the changes on the real economy looked fine for the near term, and the rising forward real yields gave a distinctly positive picture of market sentiment about the more distant future. According to the minutes of the Fed’s late July meeting: [2]

The staff’s projection for real GDP growth over the medium term was essentially unrevised, as higher equity prices were seen as offsetting the restrictive effects of the increase in longer-term interest rates. The staff continued to forecast that the rate of real GDP growth would strengthen in 2014 and 2015… [leading] to a slow reduction in the slack in labor.

By year end 2013, the same story held as in early September, but more so (Table 1, Fig. 1). The stock market was up another 12 percent, risk spreads were down a good deal more, and the forward real rate moved a bit higher. What we find remarkable, though, is that after jumping in the tantrum, the bond yields we are discussing spent the next 33 months grinding slowly back to pre-tantrum levels (Table 1, Fig. 1).

It is important to note that in between Sept. 5 and year end, market’s experienced a transitory, partial reversal of the tantrum moves (see the brief dip in Fig. 1 after Sept. 5). This wouldn’t bear mention but for the fact that it plays a role in the skittish Fed narrative. As we’ve noted elsewhere, the jobs report on Sept. 6 was disappointing, which combined with other indicators, caused the Fed to put off starting the taper at its Sept. meeting. This non-move shocked markets, leading to a brief, partial reversal of the taper moves. But the jobs picture was much less worrisome by December, and the Fed started the taper. Thus, as the taper got underway, the initial tantrum-related realignment of asset prices had been reestablished and slightly extended.

What should we make of all this? It seems pretty clear that Fed words and actions triggered[3] many of the big moves over this period. But it’s pretty hard to tell a story of the overall tantrum moves that rests primarily on news that Fed policy would be tighter than expected. The stock market was up 16 percent with real and nominal yields up sharply. The easiest story to tell is probably that market participants, for reasons that escape us, decided that in the fullness of time, the economy was headed back to a pretty pleasant normal.

So the excitable dove who remembers this period as 1937 narrowly averted needs to take another look. So too with the hawk who sees a shell-shocked Fed, cowed into holding yields artificially low ever since. By December 2013, as the Fed began the taper, longer-term yields were at their highest levels in years. And as the Fed has gradually reduced accommodation ever since, longer-term yields have ground inexorably lower and those risk spreads have risen. In the hawkish story, we suppose, a bolder Fed would have tightened more rapidly, supporting appreciably higher real and nominal yields today. Not likely.

What should we think today when people raise the possibility that a surprise tightening of monetary policy might bring on taper tantrum, the sequel? While we can’t explain what gave the initial tantrum its rosy patina, we all know that sequels can be very good (see Godfather II) or horrendous (see Caddyshack II). And we see a couple of good reasons to suspect that significant surprise tightening would be a lot rougher today. First, that 5-year forward real yield of zero was a puzzle in 2013, but it’s subsequent slow return to zero has been associated with awful productivity growth and sentiment has turned from puzzle toward stagnation—hardly the background condition for a burst of optimism. Second, is the value of the dollar. We have made no reference to the exchange rate so far, because during the tantrum period, the trade-weighted exchange value of the dollar was roughly unchanged.[4] Once again, the simplest story to tell is not one of surprising Fed tightening, but one of renewed optimism—global optimism not favoring the dollar over other currencies. But today, market participants are chewing on disappointing euro area economic outcomes and policy, Brexit, persistent anxieties about China and renewed concerns/confusion about Japan. It is difficult to imagine that surprisingly aggressive tightening by the Fed would leave the dollar’s value unchanged.

Thus, unless prompted by some very good news about the real economy, we suspect that any signal of significantly tighter-than-expected Fed policy would be met with confusion, turmoil and a hasty Fed retreat.

Of course, that’s why the consensus of the FOMC has clearly stated and demonstrated that, absent a big change in the economic outlook, it won’t be delivering significantly tighter policy. Remember that 14 months passed between the end of QE3 and the first 25 basis point increase in the fed funds rate. And 9 months later, the FOMC is only now tentatively approaching another rate increase. Given this glacial pace, even a surprise increase in the fed funds target this week should not be mistaken for appreciably tighter policy. But we have to admit that markets seem fully capable of making that mistake. Overall, any sequel to the tantrum right now seems likely to be a bad one.

But a good sequel with rising rates, a rising stock market, falling risk spreads, and a buoyant economy is also not out of the question. It seems far more likely that fiscal policy, rather than monetary policy, would trigger it. As we and others have been arguing, both U.S. Presidential candidates seem intent on delivering substantial fiscal stimulus. Indeed, around the world, it seems that austerity as stimulus may be out and stimulus as stimulus may be in. If so, it’s at least possible that we’ll see a meaningful acceleration for economic growth, underpinned by government spending, tax cuts, wall building, and so forth. As the Reagan years clearly demonstrated, combined tax cuts and spending increases can jolt the economy from a malaise.

Should that transpire, we might find ourselves thinking very differently about monetary policy and rising policy interest rates in 2017 and beyond. We can only hope.

Notes:

1. Some of you recall many FOMC members seeming pretty shaken by the immediate market response to Bernanke’s June announcement of the taper plans. In the initial response, market indicators of interest rate liftoff shifted forward in time in a manner inconsistent with the Fed’s forward guidance. This did generate great concern, but this was pretty short-lived. As reported in the July Minutes:

Sizable increases in rates occurred following the June FOMC meeting, as investors reportedly saw Committee communications as suggesting a less accommodative stance of monetary policy than had been expected going forward; however, a portion of the increases was reversed as subsequent policy communications lowered these concerns… On balance [by the time of the July meeting], [T]he federal funds rate path implied by financial market quotes steepened slightly, on net, but the results from the Desk’s July survey of primary dealers showed little change in dealers’ views of the most likely timing of the first increase in the federal funds rate target.

2. This analysis was supported by related minutes comments:

Spreads between yields on 10-year nonfinancial corporate bonds and yields on Treasury securities narrowed somewhat…

Market sentiment toward large domestic banking organizations appeared to improve somewhat…

Financing conditions in the household sector improved further in recent months. Mortgage purchase applications declined modestly through July even as refinancing applications fell off sharply with the rise in mortgage rates. [back]

3. Which is to say, immediately preceded. [back]

4. As discussed in a 2013 speech by Governor Jay Powell, the dollar did appreciate versus a number of emerging market currencies, causing considerable concern. On a broader basis, the value of the dollar was little changed. [back]