There are two parts to forecasting monetary policy: forecasting what picture the economy will present to the Fed, and forming a judgment about how the Fed will react to that picture. The first of these is pure forecasting—what will happen tomorrow? Given a macro forecast, the second mainly requires a view about the Fed’s ongoing decision framework. Insert your forecast into the decision framework and out pops a judgment about the likely course of policy.

The pure forecasting step is where the real action has been of late: the FOMC’s consensus has very steadily followed a simple decision framework for several years now. Thus, your view of where policy is going shouldn’t depend much on puzzling about the Fed and should focus almost exclusively on the economy. We’ve taken to quoting James Carville: It’s the economy, stupid.

At mid-Summer in what has been a novel year, it is probably worthwhile to do a deeper dive into economic forecasting.

Forecasting

Most analysts put great effort into forecasting, carefully analyzing myriad indicators of whether the economy is heating up or cooling off. Together, your present authors have over 50 year’s of humbling experience forecasting on Wall Street and analyzing forecasts at the Fed, and we separately came to the same conclusion: the resources poured into near-term forecasting seldom improve and often degrade forecast accuracy.

Don’t get us wrong, forecasting is a very important endeavor. Eisenhower famously said that in battle, plans are useless, but planning is everything. Similarly, we have found that forecasting is a vital umbrella activity for performing due diligence regarding myriad details in the economy. You start with a sense of ongoing trajectories, digest a wide variety of current developments and consider whether to tweak or even sharply revise your sense of the most likely snapshot going forward. It takes great discipline, however, after expending great effort in this due diligence, to remind yourself that most of the time you have been sifting through noise and that there is essentially no signal. Most forecasters yield to temptation and nudge their forecasts this way and that in response to fleeting changes in short-term indicators. Much evidence supports the conclusion that these nudges are, for the most part, counterproductive.[1]

Thoughtful institutions, including the Fed in our experience, appraise short-term indicators the way good doctors look at myriad health metrics in an annual checkup: study the numbers carefully because every now and then, you find something that is best caught early.

For example, certain big jolts to the economy elicit predictable responses. Dramatic moves in the exchange value of the dollar have predictable ongoing effects on net exports. A sharp rise in oil prices generally portends higher headline and core inflation. Production quickly bounces back from major disruptions due, say, to hurricanes or dock strikes. Large fiscal stimulus, in the short run, tends to lift output, interest rates, the value of the dollar, imports and the trade deficit. In short, some large events warrant tweaking your forecast.

Illustration: 2012—2016

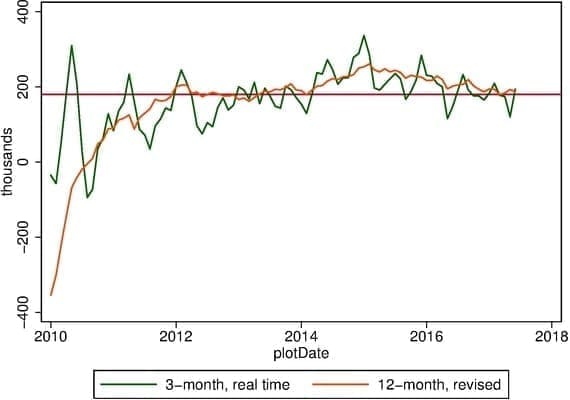

You can see an illustration of our forecasting perspective and of the history of the monetary policy debate in Fig. 1. Up through about 2012, both 12-month job gains as we understand them in today’s revised data and the real-time measure of 3-month gains provide plenty of reason for concern. But starting in 2012, the story changed. In particular, twelve-month job gains have been very steady and consistently at or above 180,000 per month.

Fig. 1. 12-month trailing job gains and 3-month trailing gains as reported in real time. Reported at a monthly-average rate, in thousands. Source: BLS via Alfred and authors’ computations.

In contrast, the shorter-term, real-time, measure has provided lots of fleeting material for both the overheating and the downward spiral enthusiasts. Three-month gains showed a major drop in 2012, and given the recent history at that point, it is probably no surprise that the Fed responded aggressively, with QE3 and the thresholds in forward guidance. In hindsight, revisions and a longer perspective have essentially removed that worrisome drop from the data. Since the start of 2013, 3-month, real-time gains have alternately provided (false) signals of boom and bust. Consistent with our perspective, however, all these wiggles seem to have been noise signifying little.

In our view, the real payoff to forecasting comes fairly rarely, when risks of a major change in the direction of the economy begin to rise notably. This happens, say, every 5 or 10 years—think 2000 or 2007. The real trick for a forecaster comes in distinguishing these signals from background noise and neither allowing the background static to drown out the sounds of the coming event nor hearing a major event in every crackle and pop in the data.

This brings us to the present, to Mr. Phillips and Mr. Trump, and to the question of whether we are now at one of those turning points.

Forecasting meets Mr. Phillips and Mr. Trump

About the time resource utilization in labor and other markets showed real gains back in 2011, we began to hear warnings of rising inflation and overheating. Those cries steadily intensified for the next several years, and by 2016 even level-headed, inflation doves[2] we’re joining the chorus.

Like most analysts, we believe in a version of the Phillips curve: at some point as resource utilization tightens, inflation and or other excesses must emerge. But we have also emphasized that economists have never had a good handle on when the symptom—tight job markets—signals the onset of the pathologies.[3]

In Six Degrees of Separation, posted May 2016, we listed six of the myriad reasons why job growth might continue on the same path for at least a couple of years with no sign of accelerating inflation. That was not a prediction that no inflation was coming, rather it was reminder that there was no sound reason to suppose that rising inflation was just around the bend. Since our prediction, steady monthly job growth of around 185,000 has continued, pushing the jobless rate down from 5.0% to 4.4%. Nonetheless, hourly wage gains registered no aggregate acceleration, climbing at a tepid 2.5% yearly pace, and the yearly inflation rate measured by the core PCE deflator actually slipped a bit to less than 1.5%.

We think we made a good non-call. When relying on Mr. Phillips, one should follow the wag’s advice to forecasters: give an outcome or a date, but not both.

And then there is Mr. Trump. In the quarterly forecast produced just after the election, forecasters had to consider the importance of the election outcome for the near-term macro forecasts. Was this one of those big events generating real signal about the macroeconomy? Major fiscal stimulus, as noted above, is one of those reliable signals, and major stimulus combined with already tight labor markets could be a combustible mixture. Like many forecasters, we had at least modest confidence that GOP control of the White House, Senate, and House, combined with the widespread GOP campaign promises of major tax cuts and infrastructure spending would bring a big fiscal boost.

Truth be restated, that seemed like an easy call. Today, of course, it looks to be incredibly off. We greatly underappreciated the cannibalistic tendencies of the Republican party and were incredibly naïve in imagining that a man of Trump’s self-declared impressive stature would be able to reach this very low hanging fruit.

So Mr. Phillips and Mr. Trump gave rise to one non-call that looks pretty good and one political call that appears very wrong.

Quick Summary of our Revised Forecast

Going forward, a blend of tax cuts, higher government spending, and deregulation might still be coming and, at minimum, would deliver a sugar high (ignoring the longer-term payback). But we no longer have those policies being adopted in our base case. Without these policies, our modal forecast shows more of the same: tepid GDP growth and steady employment growth.

And if the real economy continues in this way,[4] we continue to concur with the Fed that conditions are in place for inflation to return to fluctuations near 2 percent. When? There is still room in those degrees of separation, so there is no strong reason to believe that the weak upward forces on inflation will dominate myriad other factors in the near term. Thus, more of the same looks like a good modal forecast for inflation as well, with a bit higher and a bit lower inflation roughly equally likely in the near term.

The Monetary Policy Implications

As we approach year-end, any discussion of policy must be prefaced by the fact that a great deal may turn on who, if anyone, Trump and the rabble on capitol hill manage to send to fill the Chair and/or governor positions at the Fed. We’ll take a pass on that one just now.

As for the remainder of Yellen’s term, the Fed’s consensus has been very clear regarding the path of policy under the base macroeconomic case of continued tepid growth, steady job growth, and inflation below target (likely due to transitory reasons). We’ve been describing policy in this case as guided by two principles:

So long as steady job market gains persist, continue a gradual, pre-announced removal of accommodation.

So long as inflation remains below target, take a tactical pause if credible evidence arises that the job gains might soon falter.

Consistent with this framework, the Fed has raised the federal funds rate target 3 times since early December of last year.

The big question right now regards at what point continued low inflation might warrant a pause, or reversal, in the gradual removal of accommodation. In answering this question, it is vital that we remember that there is no simple relation between increases in the federal funds rate and changes in the degree of accommodation in financial conditions more generally. Even after the lesson of Greenspan’s conundrum, this point seems regularly to be underappreciated.[5]

Financial conditions today are arguably more accommodative than they were before the 3 recent rate increases: the 10-year government yield is down about 20 basis points over this period; the spread of Baa corporate yields over the government 10-year yield is down a further 8 basis points; the S&P500 is up almost 10 percent; the dollar has weakened by about 5 percent. We have also seen another half year of job market tightening since the December FOMC meeting. Thus, the upward pressure on inflation provided by financial and general economic conditions has increased since December in standard thinking such as that favored by the FOMC. This is true despite the increases in the federal funds rate.

(As an aside, we suspect that the forces emanating from the economy that have, thus far, neutered the Fed’s rate increases could rapidly reverse themselves in response to further Fed tightening or signs of a more robust economy. Think of the financial market spasms now called the taper tantrum. If that occurs, the earlier rate increases will, for better or worse, matter. The FOMC is, we’re confident, well aware of this possibility.)

So far, with the decline in inflation substantially accounted for by special factors and conditions remaining accommodative, the Fed’s standard MO has been to stay the course.

What precisely does this mean? We always downplay predictions of the particular timing of policy steps. The particular timing does not matter much for the economy, and can thereby reasonably be driven by minor factors that no FOMC outsider is very aware of. For concreteness, however, we’ll say that the Fed’s standard MO probably translates into no rate increase at this meeting, but another rate increase, perhaps as soon as September. Portfolio normalization will start as announced later in the year. This much anticipated step, when it comes, will not signal any desired shift in the stance of policy, only a shift in the mix of tools.

Later in the year, if the economy shows signs of faltering—e.g., if job gains or inflation drop markedly—we’ll get a tactical pause while the FOMC awaits evidence on whether the signs are mere noise or are real signal. If instead, inflation or real activity are much more robust than in the modal outlook, we’ll likely see the tightening effects of the earlier rate increases show through and, if needed, we’ll get more rate increases. In short, it’s the economy …

Notes:

1. See, e.g., Faust and Leeper’s Jackson Hole paper in 2015 and Faust and Wright’s Handbook of Forecasting chapter on inflation forecasting. [back]

2. Eric Rosengren is a good example here. [back]

3. This has been an ongoing theme. [back]

4. And presuming that Fed policy remains accommodative as the Fed has communicated. [back]

5. For a discussion of this period, see Faust and Leeper’s Jackson Hole paper. [back]