By Robert Barbera and Yingyao Hu

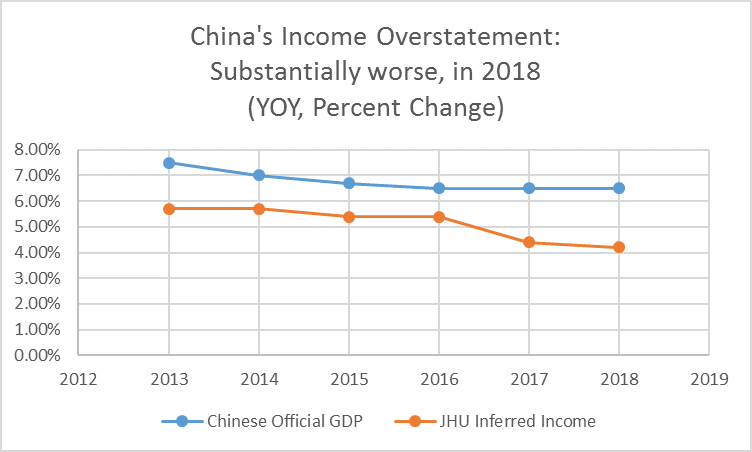

Our nighttime illumination estimate for 2018 Chinese growth, 4.2%, is roughly one third weaker than the Chinese official claim of a 6.5% climb for real GDP. In December of last year we introduced a new measure for China’s real income gains. The unique aspect of our effort reflects our statistical analyses of satellite imaging of nighttime Chinese city lighting. As we noted in our previous essay, analyses of the growth for nighttime city illumination, correctly filtered, closely mirrors the climb for national output for a whole host of countries. China, however, is a glaring exception. Gains for city lights have been systematically weaker than official estimates of Chinese real GDP growth, and this divergence has worsened over the past two years. We recently received satellite imagery for 2018. As the chart below makes clear, the divergence last year, between our estimate and the official tally, mushroomed.

A naive interpretation of our data would lead one to assert that China’s claims about real gross domestic product gains are greatly inflated. We have a more nuanced view. Other critics of official data have done bottom up analyses and conclude that China’s real GDP data greatly overstates the level of investment activity—the booming sector driving China’s growth over the past decade—a reflection of regional officials’ exaggerating the gains for construction, in an effort to claim that they have met overall growth targets.

We don’t doubt that some officials provide fanciful claims about investment rates. We conjecture, however, that a significant additional part of the mismatch between our illumination data and the official GDP tally reflects the increasingly uneconomic nature of Chinese investments in office and residential real estate. Despite soaring vacancy rates, investment continues to rise. Increasingly, however, the buildings go up, but the lights don’t go on

The Brookings paper estimates that real output gains were roughly 80% of official tallies, 2008-2016. Our mismatch suggests that real gains were only 70% of the official figure over that period. More importantly, our measure records a serious worsening of the mismatch, over the past two years.

Clearly, how one tallies investment flows is the critical issue for measuring China’s growth rate over the past 10 years. We assert that a mark-to-market approach to China’s investment flows would require ever greater depreciation of investments, immediately upon completion. Instantly writing down the value of office space, homes and condos, to get to an estimate of NET investment, for us, closes the gap between official growth rates of 6% to 7% and our tallies of 4% to 5%. If we are right about the need for ever increasing write downs, then we can also infer three things about pressures across sectors of the Chinese economy.

Imagine a nation wherein income flows to two factor inputs, labor and capital. Our restated national income figure conjectures that buildings keep going up but fewer and fewer lights go on, as utilization falls at a faster and faster rate. In such a world, the official tally of output growth might do a decent job of signaling the trajectory for wage income gains, as building were, indeed, built. The squeeze from the lower trajectory for overall income, in such circumstances, would be experienced largely by owners of capital.

This dynamic would generate growing pressure on mark-to-market evaluations of bank balance sheets, as loans to builders will be backed by investments with ever worsening cash flows. More visibly, we should see substantial increases in debt defaults. And right on cue, in the first four months of 2019, debt defaults were triple the January-April pace of 2018.

To restate for emphasis, the fact that buildings continue to be built, insulates to a degree, wage earners. In our highly stylized framework, the brunt of the hit to income streams is borne by the owners and financiers of investment.

We repeat a quote from Herb Stein. “If something cannot go on forever, it will stop.” In market based economies, when the conventional wisdom recognizes that recent investment projects cannot possibly service their debts, funding banks’ access to capital comes under heavy pressure, investment plunges and economic activity retrenches. China is different, as they have no ideological qualms about infusing banks with additional cash. Thus as long as the government can borrow at reasonable rates, it can both paper over bank losses, and it can exhort banks to continue to fund uneconomic projects. China has done just that for more than a decade.

On the face of it, one can argue that China’s last ten years’ worth of economic advance is a colossal example of the modern monetary theorists’ assertions about the extent to which governments can tap into fiscal and monetary largess. Of course Herb Stein’s dictum looms ever larger in China. Stripping away the cleansing nature of free market forces–creative destruction via bankruptcies—certainly suggests that an expansion will go on for much longer. But in the long run…