The United States has become the world’s largest oil producer. That honor is likely to vanish, and with it a lot of companies.

If so – and it is almost certain to be so if the oil price war is not promptly ended – the question will be what impact that will have on the rest of the financial system. Twelve years ago, when the subprime mortgage market was in distress, officials repeatedly noted how small that market was, and said the overall economy and financial system would escape unscathed.

They were wrong.

It was 18 months ago that The New York Times ran an article by Bethany McLean that now appears prophetic:

The problem is that the oil the U.S. is producing costs a lot, and requires massive investment to continue to grow, as new wells quickly decline in production. It is possible that Russia and Saudi Arabia both have U.S. companies in sight, and hope to drive the higher-cost producers out of business.

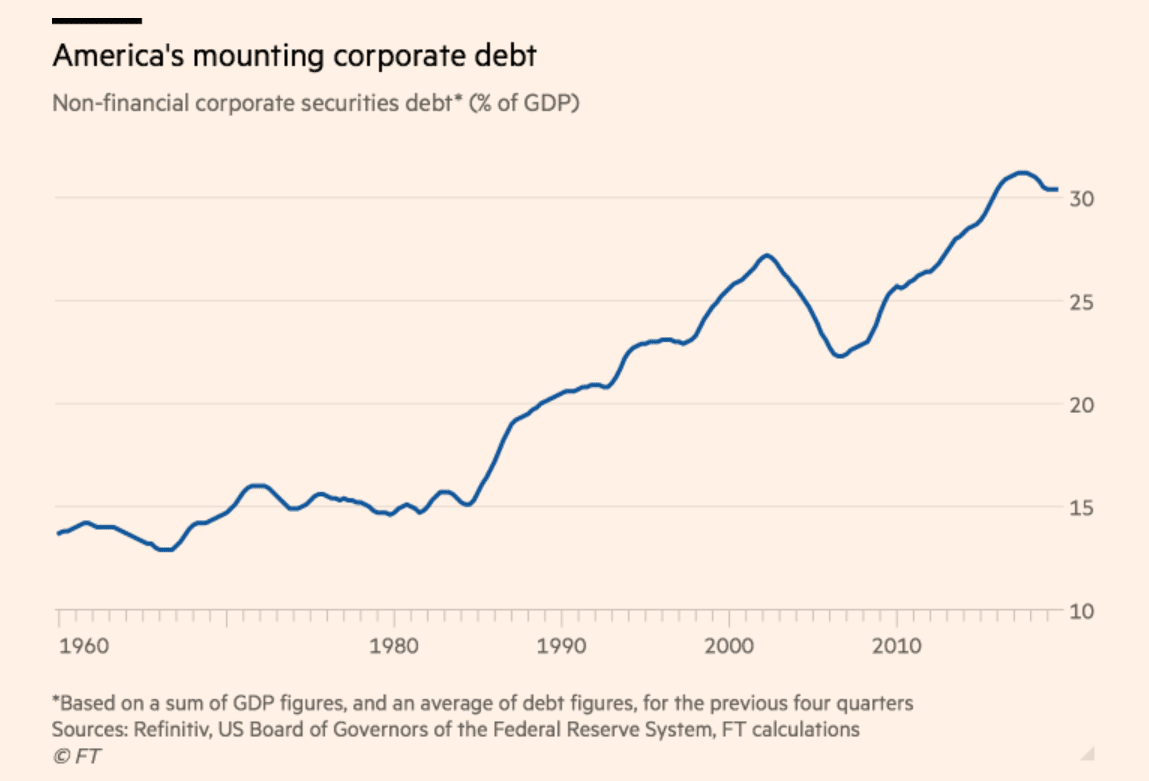

Overall, corporate debt has been rising rapidly in the United States – fueled by economic boom and low interest rates. The Financial Times recently ran this graph:

But such debt must eventually be refinanced. And, as millions of homeowners learned in 2008 and 2009, there can come a time when that is not possible.

For the banks, they may well be in much better shape now. They have more capital, and this lending binge has been concentrated more in financial markets than in banks. But back in 2008 it appeared that much of the sub-prime risk had been dispersed from the financial system, and that turned out to not be true.

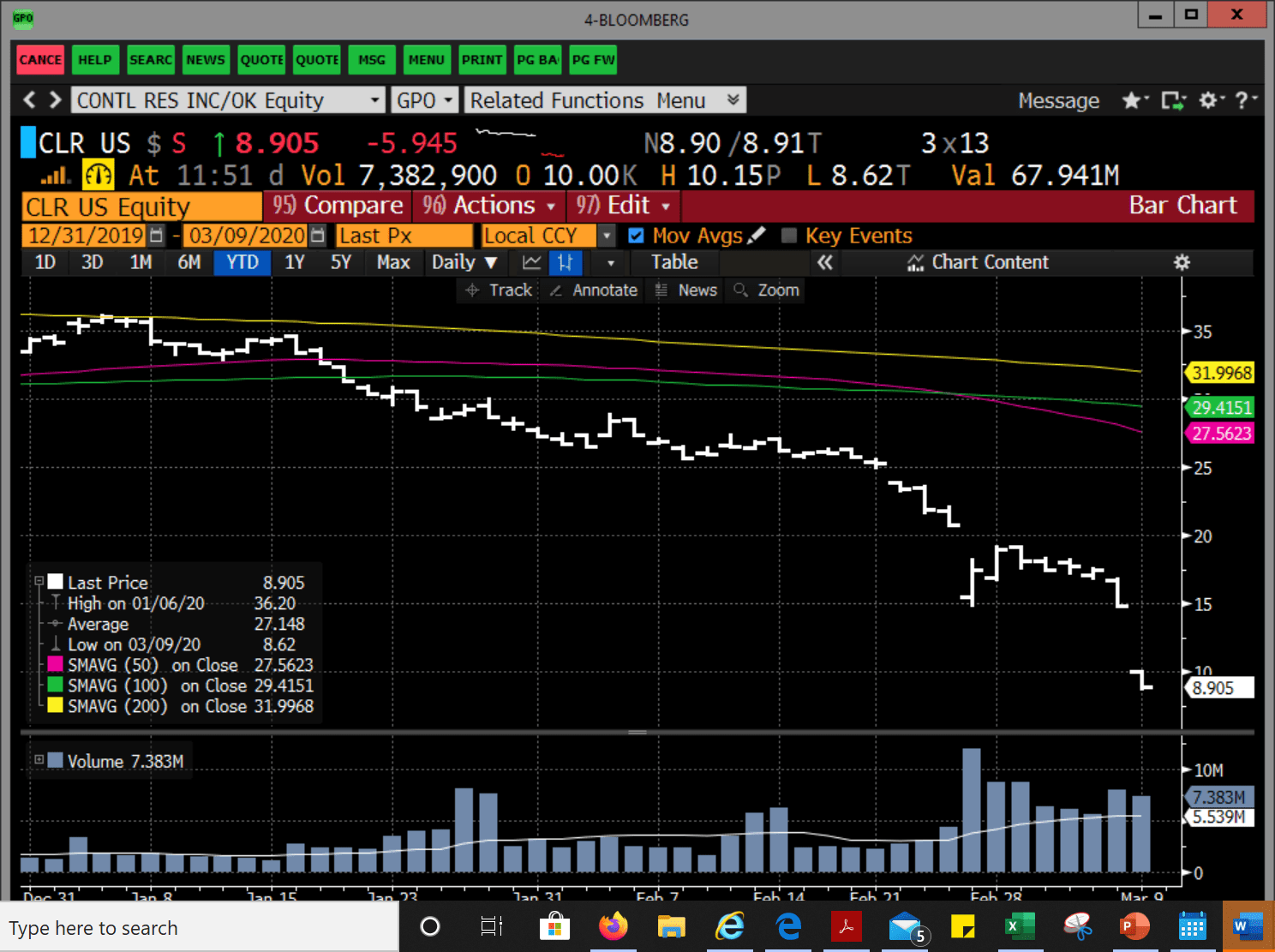

In the meantime, consider the current plight of Continental Resources, a big fracking company based in Oklahoma City – and one that, unlike some of its competitors, has not spent money on hedges to protect it from declining oil prices.

All seemed more or less okay to the financial markets a few weeks ago. Its bonds were trading around par, and its stock, while down from around $50 a share a year ago, was around $25.

Here are price charts this year for its common stock and for one of its bond issues, a $1 billion issue of 3.8% bonds, issued in 2014 and maturing in 2024. Both S&P and Fitch have the bond rated investment grade, while Moody’s has it just below investment grade. The charts go through early afternoon Monday.

Continental Resources: Bond

No one anticipated that the triggering event for a world financial crisis would be a disease that began in a market in a distant part of China. But the markets now think that is the case. We will see how resilient the U.S. financial system is, this time.