The CBO’s recent projection of a federal-debt disaster rests critically on the combination of two projections:

1. Real interest rates will rise substantially, increasing the cost of debt service.

2. Real GDP growth will remain tepid, resulting in tepid growth in tax receipts.

Either of these outcomes might plausibly occur. But both history and basic economic reasoning tell us that there is no basis for anticipating that they will both happen. And if only one of the two happens (either one), the long term debt problem is much more modest.

The U.S. Congressional Budget Office (CBO) in early February released its revised outlook for U.S. deficits and debt. The picture is alarming. According to CBO the gap between our revenue and spending—our primary deficit—closes rather nicely over the next 10 years. Nonetheless, CBO projects that as interest rates normalize, debt-service costs are destined to mushroom. Late in the period, our deficits and debt swell as the government is forced to pay much more to borrow. And in the long run? Deficits continue to rise as demographic forces swell the primary deficit and as debt service costs grow dramatically. In 2038, 25 years from now, CBO envisions debt at around 100% of GDP, nearly a 30 percentage point jump from its current level.

Relax. No need to buy shotguns and canned peas. For starters, take comfort by looking at previous CBO projections. A little more than a decade ago, CBO envisioned a decade of near perfection that was slated to deliver an accumulated $5 trillion surplus. Sadly for all of us, that proved to be a spectacularly incorrect projection. But it is an important reminder of just how wrong long term forecasts can turn out to be.

CBO, understandably, dares not stray too far from conventional wisdom about evolving economic circumstances. And it is easy to document that consensus thinking is strikingly predisposed to embrace the recent past as a blue print for the future. That is, unambiguously, what they did in 2001. And that, it appears to me, is precisely what they are doing today.

The CBO forecast, predictably, now envisions an extension of the terribly disappointing recovery that has plagued the U.S. since 2009. Five years is a lifetime for forecasters. Five years of Brave New World Boom was all it took to allow the conjuring of a $5 trillion surplus. And after 5 years of meager growth and shrinking labor participation, CBO now sees only little additional room for swift rebound and a tired long term trajectory thereafter. Laid alongside this tale of woe, again quite predictably, they attach a very traditional rebound for interest rates. Confronted with widespread evidence of real growth disappointment, CBO ratcheted down its expansion trajectory. But with no U.S. history of economic rebounds that don’t lift rates, CBO marries a traditional rate rise to their moribund real economy forecast.

Are we destined to suffer through an extension of timid recovery, followed by a meager trend trajectory for growth? It is certainly possible. Is it reasonable to expect real interest rates will move meaningfully higher in the years ahead? Of course. But is it likely that, simultaneously, we will see an extension of weak growth, no inflation pick-up, and the normalization of real interest rates? No. Instead, for a wide variety of more reasonable combinations of growth, inflation and interest rates, deficits and debt accumulation look to be meaningfully lower than current CBO trajectories.

Real Interest Rates in the Post-War Period

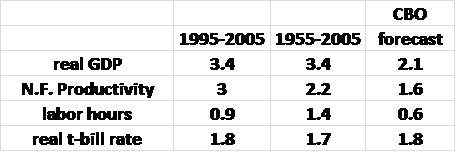

Is the CBO interest rate forecast at odds with conventional wisdom about likely prospective interest rate changes? Absolutely not. There is widespread agreement that, in the fullness of time, interest rates will return to normal. And when asked what constitutes, in normal times, a neutral real fed funds rate, 2% is answer most economists offer up. That is true among private forecasters. And that is also the view held by many Federal Reserve officials. Indeed, each of 17 Fed officials provided their opinions on the ‘longer run’ fed funds target in early February of this year. The average expectation was 1.9%, with 2% was both the median and modal value (see FRB Monetary Policy Report, February 11, 2014).

Broad sweeping comfort with 2% as the neutral real short rate is close to the reality of post war U.S. economic history (see table). But post War U.S. history was a world of a bit more than 3% real GDP growth. As the table above details, for the ten and fifty year periods ending in 2005—on the eve of the Great Recession—U.S. Real GDP growth averaged a bit more than 3%.

To belabor the point, real short rates of a bit less than 2% travel hand in hand with real GDP growth of a bit more than 3%. To state what should be obvious, if we are bound to settle into a world of limited growth and low inflation, real rates are quite unlikely to rebound to levels witnessed in the halcyon days of 3% plus economic expansions.

CBO’s Incorporates of Plunging Participation

Why capitulate to the notion that we destined to grow slowly? CBO now believes that the labor market will be moribund state for the long haul. Their major downward real GDP revision, 2014-2018, reflects their embracement of the recent plunge for the jobless rate. As we all know, a major part of the fall for unemployment reflects the striking drop for labor force participation. CBO now has joined analysts at the Bureau of Labor and Statistics, and believes this drop is permanent. Accordingly, they look upon this as evidence that much of the output gap is now filled and there is less room to grow before we run up against capacity constraints.

Is the decline for participation structural, a development independent of the Great Recession? It may well turn out to be structural, as a persistently lackluster economy limits job opportunities over the long haul. But as the above chart reveals, it is almost impossible to argue that the fall in participation largely reflects demographics. Around 83% prime age workers identified themselves as in the labor force, from 2003 through 2007. As the economy swooned so too did the participation of this group. To state the obvious, 25 to 54 year olds are not retiring early.

Lower Potential GDP and Less Near-Term Economic Growth

The capitulation to a much smaller labor force led CBO to dramatically cut its measure of the U.S. output gap. In turn they sharply reduced their estimate for real growth, 2015-2017, and at the same time allowed the U.S. economy to achieve full employment in 2018:

And in the end? Full Employment Translates to Normalized Interest Rates:

But look at the change in employment growth!

I spent much of my career in finance. Speculators in the U.S. bond market, over that 30 year period, revealed to me a profound interest in the pace of employment growth. Grudging increases in payrolls, in low inflation circumstances, were almost always accompanied by falling interest rates. For me, therefore, the most telling disconnect embedded in the CBO forecast, was the willingness to simultaneously slash their employment growth forecast and modestly raise their forecast for long term interest rates.

The Error That Keeps on Giving

In 2001 CBO asserted Americans were to be blessed with 10 years of strong productivity, healthy employment gains and record levels of labor force participation. Inexplicably high individual income tax payments would persist. Bear markets, recessions and wars would all stay away. Over the 2001-2011 time-frame we were set to collect trillions, ending the forecast period, in 2011, with a budget surplus of more than 5% of GDP. There were, of course, skeptics, at the time. I was one of them (see The Bubble Budgets, Financial Times 2001). But the great majority embraced the super surplus story. It didn’t require anyone to dream dreams. All you needed do, to believe in these riches, was to imagine that the next ten years would, in most respects, approximate the last five years. A steady as she goes forecast landed you in Shangri La by decade’s end.

Of course that is not exactly how things worked out. Instead we witnessed a stock market crash, wiping out the inflated individual income tax payments, a recession, ill-timed tax cuts, two wars, a spectacular financial crisis and a big recession. In short, almost everything that could drive the deficit higher came to pass. The end result? Deficits reappeared and then soared. The 2011 deficit was over 8% of GDP—quite a miss, relative to the 5% surplus expectation championed in the 2001 outlook.

The 2014 forecast, I think, suffers from the same kind of myopia that helped create the 2001 outlook. The forecast embraces a paltry growth trajectory. Why? Powerful reasons are given, but they all amount to elaborations of the same simple linkage:

We expect a disappointing backdrop, because the backdrop for too long—five

years—has been disappointing.

In effect, CBO is saying, that notwithstanding a 50 year history of 3% real growth for the U.S. economy, the last five years are sufficient to allow them to assert that those longstanding trends are now a thing of the past. So just as CBO dismissed worries about excessive options income, the ineluctable arrival of recessions and a myriad of other things as they promised a $5 trillion boon, they now dismiss the prospects for any meaningful recovery and project a dismal backdrop as far as the eye can see.

In 2001 I was adamant that the vision of eternal bliss was bound to be very wrong. Indeed, forecasting that eternal perfection was unlikely was about the easiest pronouncement I ever made. In current circumstances, I cannot say I KNOW CBO’s pessimism on growth is unfounded. The point, however, is that the pessimism they champion on the deficit and debt outlook, is almost certainly unfounded. And that, of course, is because the debt explosion is almost entirely a product of the mismatch they have with dismal growth and normal real interest rates.

The CBO effort is therefore captive to a much more insidious computation. Again, for emphasis, the forecast embraces a traditional rise for interest rates, notwithstanding no climb for economic growth. I guess the charitable thing to say is that, having no evidence that things should be different for interest rates, they impose a ‘more of the same’ interest rate forecast—a move to a 1990s invented Taylor Rule neutrality. And lo and behold we are in a debt service crisis.

But the crisis disappears if interest rates reconcile themselves with the rotten real economy outcome. Likewise the crisis evaporates if real growth returns to a more traditional trajectory. My own tastes lean toward the second notion. An Irish colleague of mine at Johns Hopkins thinks the pessimism on the economy is justified. We like to think our different biases reflect stereo-typical differences between American and Gallic sympathies. But we completely agree on the point of this essay. Deficit and debt possibilities are much less threatening if we demand coordinated opinions about interest rates and real economy trajectories.