Just before the release of the FOMC’s Survey of Economic Projections (SEP) in December, I posted a piece saying that the dots would reveal nothing and arguing that, by design, the dot plot is not likely to help us understand policy. My main critique is that the dots convey the range of opinions, but shed no light on how the differences will be resolved. Shortly after 2 pm yesterday, Ross Margolies, a steadfast (and succinct) supporter of the CFE, emailed: I thought the dots meant nothing.

Good point. My earlier comments were wrong in neglecting an important case: the dots are informative when they are tightly clustered. For example, over the 3-year history of the dots, essentially everyone on the FOMC expected rates to stay at zero at least through the first year reported in the SEP, and the SEP very effectively conveyed that unity.

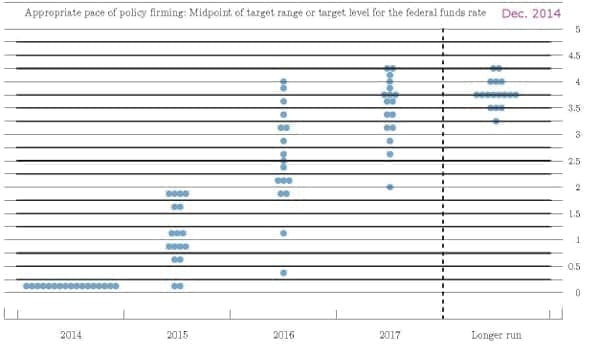

It is also true, that there tends to be much less dispersal in short-term views about appropriate policy than in longer-term views. Indeed, that former unity about zero rates in the near-term is an example of this and is illustrated in the December SEP’s current-year dots.[1]

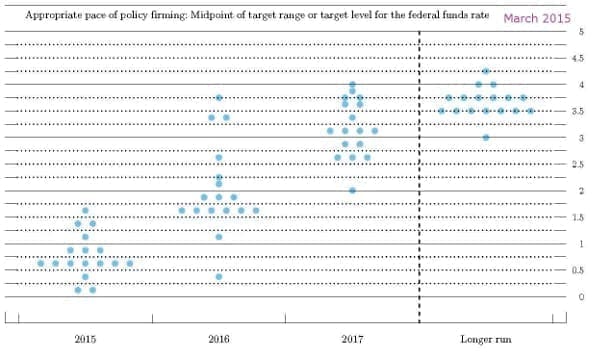

Yesterday’s SEP was the first time that the current-year dots were not clustered at zero and so we got an idea of the dispersal of views regarding policy about 9 months in the future. It turns out, that the views of policy are fairly tightly grouped.  Seven dots are in the 50 to 75 basis point bucket, three a bit lower, and three a bit higher. This conveys what we might call a Committee view that (in the modal outlook) appropriate policy involves about two 25 basis point increases in the range for federal funds rate by year end.

Seven dots are in the 50 to 75 basis point bucket, three a bit lower, and three a bit higher. This conveys what we might call a Committee view that (in the modal outlook) appropriate policy involves about two 25 basis point increases in the range for federal funds rate by year end.

Note that the dots for 2016 remain much more dispersed and subject to the earlier critique. That dispersal comes from a mixture of different views about the outlook and about the appropriate pace of tightening in light of the outlook. President Mester—who helped shape my views on these topics when we were both staffing the FOMC’s communications subcommittee—recently made similar comments about the SEP and suggested some SEP improvements. (More generally, let me emphasize that I don’t think there is anything I’ve said about the SEP that has not been considered by Fed staffers.)

It is interesting to think about the current-year dots as the year passes. In September the FOMC participants will be making a statement about policy 3 months in the future, whereas in March, the shortest horizon is 9 months. This strikes me as likely to be a source of some problems. Does it make sense for policymakers to provide information about the very near-term path of policy in the fall, but not in the spring?

More importantly, it may not make much sense for policymakers to ever provide the near-term forecast. In my perception, a major communications struggle of the FOMC has been to get observers to focus not on the immediate but on what matters most for the economy, the overall stance of policy over the next year or more. I suspect that reporting a 3-month policy projection each September would lead to an annual feeding frenzy of short sightedness.

It probably would make more sense to hold fixed the horizon over which the path of appropriate policy is reported. That is, in each SEP, FOMC participants might report their views of appropriate policy, say, 12, 24, and 36 months in the future. This would convey the modal path of the overall policy stance[2] without changing the nature of the forecast as the year progresses. A less complete fix would be to simply drop the current-year dots in the September and December SEPs.

In any case, good point Ross: when not dispersed, the dots are informative.

Footnotes

1.No matter how hawkish or dovish the FOMC participant, participants very generally do not think it would be appropriate for policy to jump abruptly to a new stance–unless conditions change abruptly. Never forget that data dependent clause. [back]

2.At least if dispersal were minimal. [back]