In a recent Financial Times article, Faust notes:

[A] growing chorus of voices as diverse as Donald Trump, the Republican candidate for the presidency, and Martin Feldstein, former chief economic adviser to president Ronald Reagan, and now a professor at Harvard, are demanding that the Federal Reserve aggressively tighten monetary policy. Mr Trump’s reasoning is hard to discern, but Mr Feldstein makes a traditional case for why job gains have become a dangerous thing. With the overall unemployment rate near the historically low level of 5 per cent, the argument goes, job growth must slow lest the labour market get too tight and prompt a surge in wage and price inflation. According to the Fed’s minutes, some version of this argument has considerable support among the central bank’s policymakers.

The very strong case against this position is just one manifestation of a point we’ve been arguing for some time. In Six Degrees of Separation, we labeled this a policy of preemptive unemployment and argued that nobody understands the jobs-inflation link well enough to justify preemptive unemployment at the current time. Reflecting on employment trends over the past year provides a potent and unsettling illustration of our point.

Six degrees of separation over the last four quarters

Over the four quarters ending in September 2015, job gains averaged about 200,000 per month—a bit more in the establishment survey, a bit less in the household survey. With the labor force rising by only about 50,000 per month, the jobless rate fell from 6.1 percent to 5.2 percent.

| average monthly gains (thousands) | unemployment | |||

| period | payrolls | household empl. | labor force | rate change (%) |

| 2014:Q3–2015:Q3 | 236 | 176 | 52 | 6.1 to 5.2 |

| 2015:Q3–2016:Q3 | 203 | 213 | 194 | 5.2 to 4.9 |

Table 1. Labor force, job growth, and the unemployment rate. Source: BLS via Fred, authors’ calculations.

Over the four quarters ended September 2016:Q3, the job gains continued at the pace of about 200,000 per month. However, unlike the previous year, the jobless rate barely budged. Instead, the growth in the number of people with jobs was met almost one-for-one with people joining or re-joining the work force. The unemployment rate fell only modestly.

Labor force participation is just one of those six degrees of separation that has historically confounded the link between jobs and inflation. There is plenty of space for another year and more of labor force gains in the vicinity of 200,000.[1] Or one of the other degrees of separation could kick. For example, we could see a jump in labor compensation with no acceleration for inflation. By the way, that’s another way of saying that workers might receive a real wage increase.

Six Degrees of Separation and the African American Jobs Recovery

As Faust argued in the Financial Times piece, a potent additional illustration of what’s at stake in these questions comes from drilling down a little further in the jobs data. We find that the jobs recovery in this expansion has been decidedly uneven across color lines.

The jobs rebound for African Americans in the first several years of the recovery was much slower than that for whites. And the African American employment recovery has, however, gained real steam recently.

The most recent 12 months provides a stark picture. Over the last 12 months, the white unemployment rate was unchanged at a healthy 4.4 percent. In contrast, the unemployment picture for African Americans a year ago remained bleak, with the jobless rate at 9.2 percent. The last year saw welcome progress, as the unemployment rate fell sharply and about half a million African Americans joined or re-joined the labor force. Nonetheless, the African American jobless rate today remains at a punishing 8.3 percent.

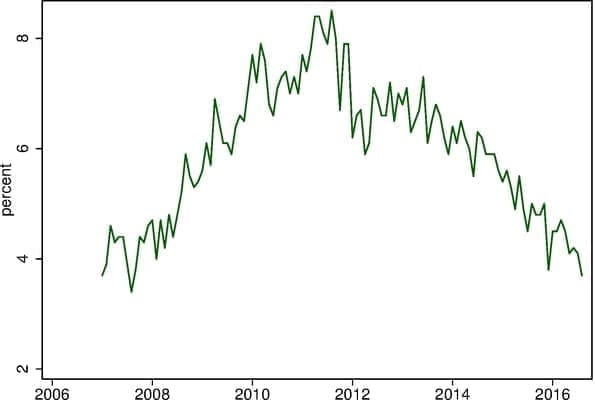

The evolution of the difference between black and white unemployment over the crisis and recovery paints a more complete picture (Fig. 1). This excess of unemployment for blacks over whites is somewhat volatile month-to-month, but fluctuate in the range of 4 percentage points in late 2007, just before the recession. The differential jumped to more than 6 percentage points by June of 2009, which is when the NBER dates the end of the recession. The differential kept climbing through 2011. The differential then came down but stayed above 6 percent.

As 2015 dawned almost 6 years into the recovery, there had been essentially no progress closing the extra two percentage points of black-white unemployment differential that that opened up during about a year and a half of recession.

Fig. 1. The difference between the African American and white unemployment rates. Source: BLS via Fred, author’s calculations.

Policy Implications?

Against this backdrop, those worried about overheating remind us of history’s lesson that inflation policy must be forward looking. True enough. History provides numerous examples of creeping inflation that gained momentum and ended badly. But inflation is still flat-lining below the desired level, and has yet decisively to make the long-desired turn upward toward 2 percent.

History provides other clear lessons as well. In particular, because of those six degrees of separation, no one has ever found a way to reliably predict a rise in inflation based in the state of the labor market. Eric Leeper and Faust document this historical point in their Jackson Hole paper from a year ago, but the most relevant history is the past seven years. Over this period, Fed forecasters have consistently over predicted inflation based on their assessment of labor market conditions and other factors.

It is undoubtedly true that at some point as job gains continue, pressure on inflation will build. And we are probably nearing that point. But there is no credible basis on which to rule out another year or 18 months (or perhaps more) like last year. It’s time to admit that nobody has a very good sense right now of when more people getting jobs will become a dangerous thing.

Up until recently, the Fed has been removing accommodation at a very gradual pace amounting to about one small step a year. A rate increase by year-end would be consistent with this pace. Doves may complain, but it would be quibbling to argue that this is too fast. Significantly increasing the pace of tightening at present based on appeals to labor market tightness, however, is not justified at this time.

Defogger: An ongoing theme of this blog is the fog of misunderstanding that surrounds Fed policy. And we aspire to minimize our own contribution to this fog. Thus, we want explicitly to discuss two misimpressions this post could foster.

First, while the jobs-inflation argument is important, it is not the only thing that is important for policy at present. We can still have a rousing debate about financial stability, international conditions, other distortions arising from persistently low rates, and so forth. We are questioning deliberately slowing job growth at present to ward off inflation pressures.

Second, we agree with Yellen that a ‘whites of their eyes’ approach to inflation would be risky. But we are arguing that, as of now, we’re barely even seeing their shadowy outlines on the horizon.

Notes:

1. For example, suppose you accept the BLS population projections by age cohort, and you allow age cohort participation rates to rise at the same pace as they did over the four quarters ending in Q3:2016. This allows three more years of monthly labor force gains of over 200,000. More conservatively, if you freeze participation rates for those 65 and over, and only repeat participation gains for the cohorts younger than 65 years old, you still register two years of monthly labor force gains of 170,000. And in this scenario, the participation rates for these cohorts remain well-below pre-crisis peaks. [back]