As a holiday sweet in Dec. 2015, we produced an Onion-style Fed watcher analysis of the coming FOMC. One key insight went roughly as follows: Our contacts suggest widespread support on the FOMC for permanently including in the FOMC statement the claim that inflation will run below target due to recent transitory factors. Not Onion worthy, perhaps, but a year and a half later, as inflation once again reverses a modest upward climb, this remains the joke that keeps on giving.

Some Fed watchers have been arguing that a troubled FOMC will struggle with how to react to recent inflation softness. Nope. The FOMC has made clear in words and actions over the last few years that policy plans will be largely unaffected by modest drops in inflation, so long as the moves do not suggest ongoing and more pronounced declines.[1] However sound this practice was over the past few years, it is surely more sound today: the rate of resource utilization has moved progressively higher, and, in almost anybody’s reasoning, this lessens any risk in ignoring transitory slips in inflation.

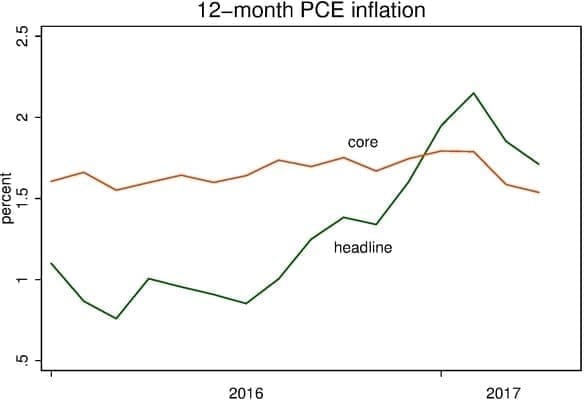

There is no mystery in recent inflation behavior

Taking as given that Phillips curve reasoning is correct at some level, we have from the inception of this blog pointed to overwhelming evidence that the jobs-inflation link gives rise to only weak forces, forces that can be swamped for years at a time by myriad other factors.

For example, back in 2014 when folks were also straining to see a rise in inflation, our post If you just squint… pointed out that shifting differences in the behavior of goods versus services inflation can clearly dwarf other forces. In Six degrees of separation, we listed several of the myriad factors that can short-circuit, for a considerable period, the relation between a tight labor market and rising inflation. In Surely we’re behind some curve, we reviewed the fact that inflation forecasts that exploit real-time measures of labor market tightness have never been of any value. Our titles are, of course, meant to tweak the many analysts who evince faith in a tight labor-market-to-inflation link.

Ruling out willful self-delusion, there is no excuse for surprise when Phillips curve reasoning fails to explain inflation movements—except over very long periods.

The policy implications?

The historical evidence is very consistent, we believe, with three propositions:

At some point as labor markets tighten, upward pressure on inflation coming from the labor market will ultimately dominate other factors and show through in rising inflation.

Partly because of challenges measuring labor market tightness, we have no reliable way to gauge the impetus to inflation coming from the labor market at any given time.

Even if we could reliably assess the inflation pressure coming from the labor market, myriad other factors would thwart our ability to make reliable predictions for inflation except over longish horizons.

The policy implication of these facts is simple: to get inflation up, keep pushing until inflation goes up.

We’d all like greater precision than that, but nobody can reliably provide it. And the consensus of the FOMC, in our view, is well aware of all this. The policy that the consensus of the FOMC has been following is to ignore the wiggles, but to maintain policy accommodation until it is very clear that inflation will return to fluctuating in a range centered on roughly 2 percent.

Why has the FOMC been raising the federal funds rate and planning portfolio normalization?

History’s lesson is to keep pushing until success. Despite the cautious and gradual steps the Fed has been taking toward policy normalization there is little question that Fed’s policy is consistent with this lesson. More specifically, the increases in the federal funds rate to date have been accompanied by many other changes in the economy that make it arguable whether financial conditions have, thus far, tightened appreciably at all. Right or wrong in the strength of the push, policy is currently consistent with ‘keep pushing.’

To be clear, we are not addressing whether FOMC policy is ideal in any sense. Expert opinion varies on whether the FOMC should have worked harder to promote upward inflation pressure, and we’d have come down on the side of pushing harder earlier. But nobody’s individual view is, or should be, of much significance. Consensus policy emerges from an FOMC that is deliberately chosen to represent a broad range of views—including views more dovish and far more hawkish than our dovish-side-of-center views. The policy clearly articulated and delivered so far on behalf of the consensus strikes us as a reasonable compromise among folks with thoughtful but varied opinions.

Bottom line

Unless the FOMC announces a profound shift this week (we doubt it), the consensus will, as usual, ignore wiggles in inflation, but they will continue promoting conditions that will ultimately push inflation up. It seems to us quite likely that the job is nearly done and that inflation will be headed upward. If, however, several months from now inflation softness persists, the FOMC will once again take up the question of whether some additional push is needed.

And in the end (barring crazy outcomes in the appointment of Fed leadership), policy will keep pushing and inflation will return to 2 percent—after those pesky transitory forces abate.

Notes:

1. This does not deny that there could be some energetic debate in reaching this inevitable conclusion. We regularly note that, as in classical Greek tragedy, the fact that the ending is largely inevitable is fully consistent with entertaining drama along the way. [back]