The outlook for growth in employment and corporate earnings over the next few years is headed down.

The problem is not what the Federal Reserve will do, or what a Democratic (or Republican) Congress is likely to do, or the possibility of a mushrooming trade war. It is the unsustainable nature of what has caused the good news this year.

Job growth is going to have to slow, and corporate profits cannot keep rising as they did in 2018.

The economic growth has been impressive. President Trump’s term in office has gotten off to the best start of any presidential term in this century, at least as measured by GDP growth. It is an accomplishment that some commentators have been reluctant to credit to the president, but it now seems clear that his policies played a major role in stimulating growth, particularly this year.

But that growth is not coming in the way the Trump administration forecast, and it is unlikely the growth — particularly in employment — can continue for much longer.

The job numbers reported Friday showed that the economy has gained an average of 213,000 jobs in the first ten months of the year, while the unemployment rate has fallen to 3.7%.

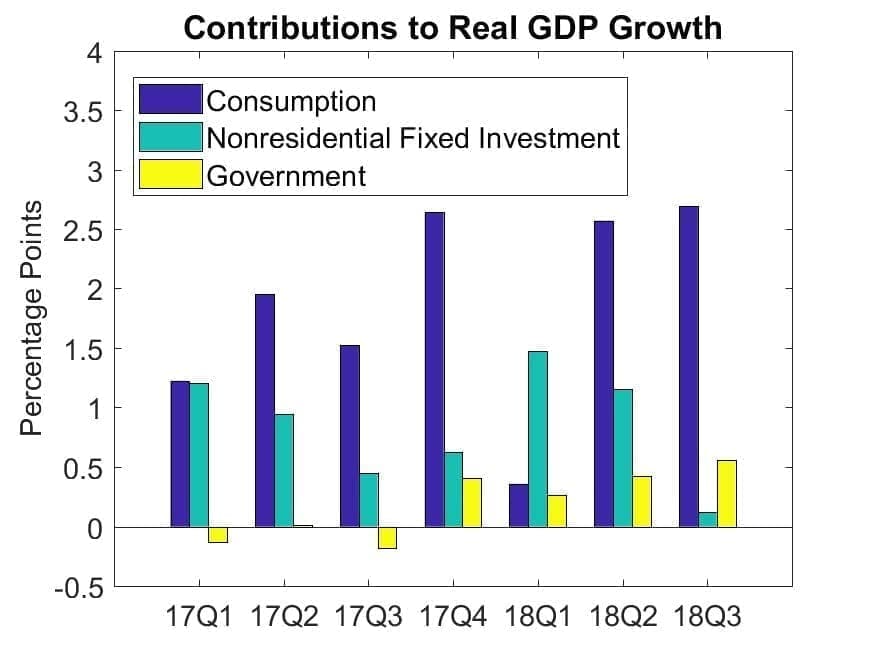

Real GDP rose at an annual rate of 3.0% during the first six full quarters of the president’s term — beginning in the second quarter of 2017 and continuing through the third quarter of this year, according to preliminary estimates released last week.

That is the best beginning to a four-year presidential term since Bill Clinton’s second term in 1997-98, and the best for any Republican president since Ronald Reagan’s second term in 1985-86.

The president’s two primary economic moves – the tax cut and his threatened trade war – each played a role in the growth.

Fiscal stimulus, we teach our undergraduates, is likely to elevate the short run pace of economic growth. The 2018 to-date response has registered a textbook response.

Which textbook? Sadly for the storytellers at the White House Council of Economic Advisors, the acceleration looks quite Keynesian. When the tax cut was enacted, great store was placed on the potential for a big acceleration in business investment, leading to a leap for the growth rate in labor productivity. Instead we have witnessed a leap for consumer spending, a faltering pace for business equipment investment and no significant change in productivity. The principal strength for business investment, oil well drilling, was already in train, and reflects the rebound for crude oil prices.

The stock market rose nicely early this year, as equity investors were showered with earnings reports describing large gains in after-tax profits. Revenues rose as the fiscal stimulus kicked in, pushing up pre-tax profits, and the tax law meant less had to be set aside for Uncle Sam.

Since the business tax savings did not go into investment, or, by and large, into increased wages, where did they go? Many went into share buybacks. Since most shares are now owned by institutions, it should have come as no surprise that the institutions reinvested the money. By the time it peaked in late September, the S&P 500 was up almost 10% for the year. A month later, all those gains were gone.

The trade war effect is less obvious, but nonetheless real. Tariffs are taxes paid by buyers of the goods, and an expectation of an increase can be expected to cause increased buying, and reported economic growth. That seems to have happened both in the United States and abroad, as buyers feared both higher tariffs on United States imports – imposed by the Trump administration – and on U.S. exports, imposed by other countries in retaliation.

But that stimulus had to be temporary. Sales that would have been made later happened sooner, and therefore were not made when they otherwise would have been.

In the current earnings season, companies are scaling back investor expectations. We think that is simply the beginning of a needed adjustment to expectations for profits growth over the next few years. Barring a second slashing of corporate taxes, there will be no gains due to less money sent to the government. There is no way to know how a trade war will play out, but some companies fear they will be casualties.

Much more important, at some point investors will have to come to grips with the fact that the top line growth rate for the U.S. economy is bound to slow, given its current dependence on well-above-sustainable growth for employment.

Are we being too pessimistic? We certainly acknowledge that productivity gains are nearly impossible to forecast. So a spontaneous surge, despite the absence of the hoped for surge in investment, cannot be ruled out. But absent that kind of event, we dismiss as nonsense the notion that today’s top line trajectory can continue, with strong jobs growth as one of its key inputs.

In our post Oct. 5, we pointed out that extending the present trajectory to the eve of the next Presidential election would put the jobless rate at 2.7%, a rate we saw as quite unlikely to come into view. Shares, in theory at least, discount the long term, which is why analysts often offer 5-year earnings growth expectations. So we note that a 5-year extension of 2018 trajectories would put the jobless rate at 0.7%. Anyone willing to wager about that eventuality can contact us, we will give you great odds. And, to state the brutally obvious, there is a zero bound issue.

To state an additional obvious point, falling joblessness does shift negotiating leverage to workers from managers, irrespective of discussions of the slope of today’s Phillips curve. Amazon’s decision to raise hourly pay will certainly be oft repeated if there is a steady fall for joblessness from today’s level.

This week the government reported that wages in the private sector were 3% higher in the third quarter than they had been a year earlier. That was the largest annual increase in a decade.

Of course, a surge of available workers could help to offset such wage pressures. The only possible source of such a surge in immigration. President Trump has made his position clear on that.

In sum, without any mention of central bank decision making or mushrooming trade tensions, we see the zero bound for the unemployment rate, superimposed upon margin pressures, as sufficient to force a rethink of prospective earnings growth.

Herb Stein, the chairman of the Council of Economic Advisors under Presidents Nixon and Ford, once observed that “If something cannot go on forever, it will stop.”

We agree.