Bob Barbera and Jonathan Wright

There is much excited talk in the press these days about the rise in ten-year yields to 1.5 percent and the rise to 2 percent for the breakeven inflation rates expressed when we comparing Treasury nominal and TIPS yields. The bond vigilantes are back! Another Great Inflation around the corner!

It is true that both ten-year yields and breakevens are well up from their lows last summer when it looked like the US was stuck at the lower bound for a long time. But by longer-term historical standards 1.5 percent is a strikingly low yield, a country mile from a yield that suggests a return of the bond vigilantes. Quite similarly, five-to-ten-year inflation compensation at 2 percent, relative to the 20-year history of these returns, remains at the very low end of our experience. Yes, rates are up some. But they remain at historically low levels, levels that suggest continued worries about faltering economies and tame inflation.

Indeed, we all should welcome the rise for nominal yields, real yields and inflation compensation. Their collective rebound is nothing more than a heartening shift from fears of a prolonged U.S. slump, to increasing willingness to imagine that robust U.S. recovery could well soon arrive (see our post of 1/9/21).

If we think of inflation compensation as just measuring inflation expectations, then the level of five-to-ten-year inflation compensation would say that CPI inflation is expected to be 2 percent from five to ten years hence. Translating that into the Fed’s preferred inflation measure, PCE inflation would be running at roughly 1.6 percent, still below the Fed’s target. And recall the Fed has been quite vocal about their frustration with having been under target, most all of the time, since 2009.

It is also important to remember that inflation compensation, embedded in financial instruments, is not the same as inflation expectations. Most of the time since the creation of U.S. TIPS, inflation compensation has proved to be higher than either econometric or survey forecasts of inflation expectations Thus, so far, the rise for inflation compensation gives no indication that actual inflation levels, will turn out to be unsettling for Fed policymakers. If anything, a literal reading of current levels suggests a continuation of inflation below target and more work to be done to drive inflation expectations up.

That said, what explains the rise for inflation compensation, to date? Much of what has changed since last summer is about tail risks. Last summer, not at all surprisingly, people genuinely feared that the US could fall into a permanent crawl, mirroring Japan’s experience. Now, amid growing confidence of big stimulus and defeat of COVID-19, there is emerging angst about the risk is of an overshoot in inflation.

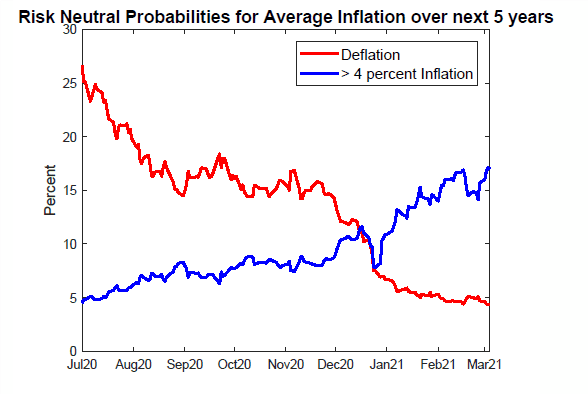

Can we validate the notion that tail worries have flipped? There is a market in inflation floors and caps which allows researchers to measure the risk of deflation or inflation exceeding 4 percent. This market was quite active about a decade ago and was discussed by Kitsul and Wright (2013). This market has since become much less liquid as fewer investors foresee extreme outcomes for inflation–but it is still operational.

The chart below shows the risk neutral probabilities of deflation or inflation exceeding 4 percent over a five-year horizon since last July. They are derived from inflation floors and caps. The probabilities themselves both seem implausibly high to us, but investors have long been willing to pay premia in this market to hedge against tail risk. The thing that is striking is that the probability of deflation exceeded that of higher inflation last summer, and now things have flipped. This would in turn be quite consistent with the idea that last summer, quite unusually, negative risk premiums played a significant role in the fall to super low breakeven inflation rates for TIPS/Treasury note comparisons. We conclude that the rebound for breakevens, to a large extent, reflects a flip back to positive risk premiums.

The bottom line is that yields and breakevens, even at quite a bit higher levels than today would still constitute unmitigated good news for the Fed and the economy—though perhaps not for stock prices. The backdrop for most of last year of a surging stock market, amid carnage on Main Street was dumbfounding to many. Some role reversal could simply be looked at as a healthy squaring up of asset markets and underlying economic and financial fundamentals.