The Pandemic recession lasted two months, the National Bureau of Economic Research decided this week—more than a year after the supposed end of the recession in April 2020. That is the shortest recession ever, according to the NBER, which has a list of 34 recessions going back to 1857.

But this recession made up for its brevity by its depth. To calculate how bad recessions were since World War II, we looked at how much output was lost during each downturn. Our methodology concludes that the 2020 recession ranks as the second worst, not quite as bad as the 2007-2009 downturn, but worse than significant recessions in the 1950’s, 1970s or 1980s.

It is worth understanding that the NBER thinks a recession is a period when the size of the economy, adjusted for inflation, is declining. When the economy starts growing again, the recession is over – whether or not that growth brings the economy back to the size it was before the downturn.

This recession may have ended last April, but the American economy, as measured by the real, or inflation adjusted, gross domestic product, at last report was still below where it was in the final quarter of 2019, before the Pandemic caused the economy to shrink rapidly, if briefly. It is expected that the first estimate for second quarter GDP, to be released July 29, will show it has regained the lost ground.

Economists, back in the day, spoke of recessions/recoveries/expansions. Using that frame, the 2020 recession ended, 2020:Q2, but recovery, not expansion, define the next 3 quarters. Assuming a rise of 4% or more, in the just past quarter, and only now is the U.S. economy expanding.

To compare cumulative lost output throughout the recession and recovery period, we looked at the amount by which the flow of quarterly output was below its pre-recession peak. We summed these shortfalls for each quarter before real GDP achieved a new high. We tallied these totals as a percentage of the previous peak. Thus, we continue to add up shortfalls well after the recession is officially over, recognizing lost output until the economy has returned to its old high[1].

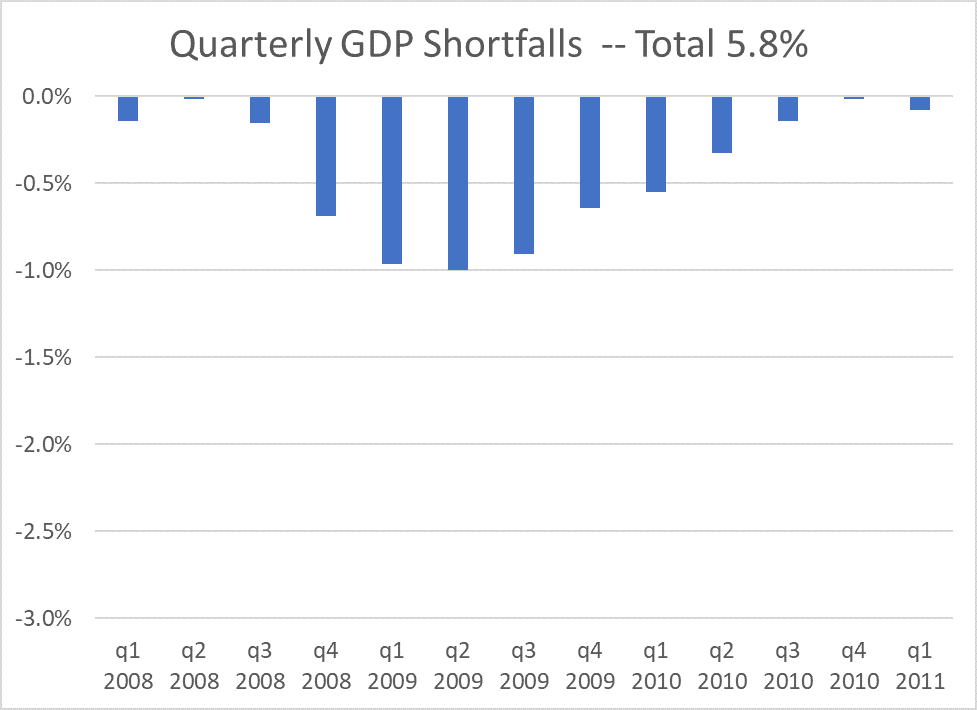

The worst postwar recession, using our metric, was the one that officially began in December 2007. The official measurement says that recession ended in June 2009, but the economy did not make up all the lost ground until the second quarter of 2011.

The worst quarter saw GDP just 1% below the old peak – but the 13 quarterly shortfalls add up to 5.8% of the old peak. In 2012 dollars, the American economy would have produced $886 billion more than it did over those 13 quarters, if the GDP had just held steady.

A 1% quarterly shortfall may not seem like much, but it was the worst quarter for the economy since World War II. It meant that the production shortfall in the quarter was equal to 1% of the entire yearly production at the pre-recession peak rate.

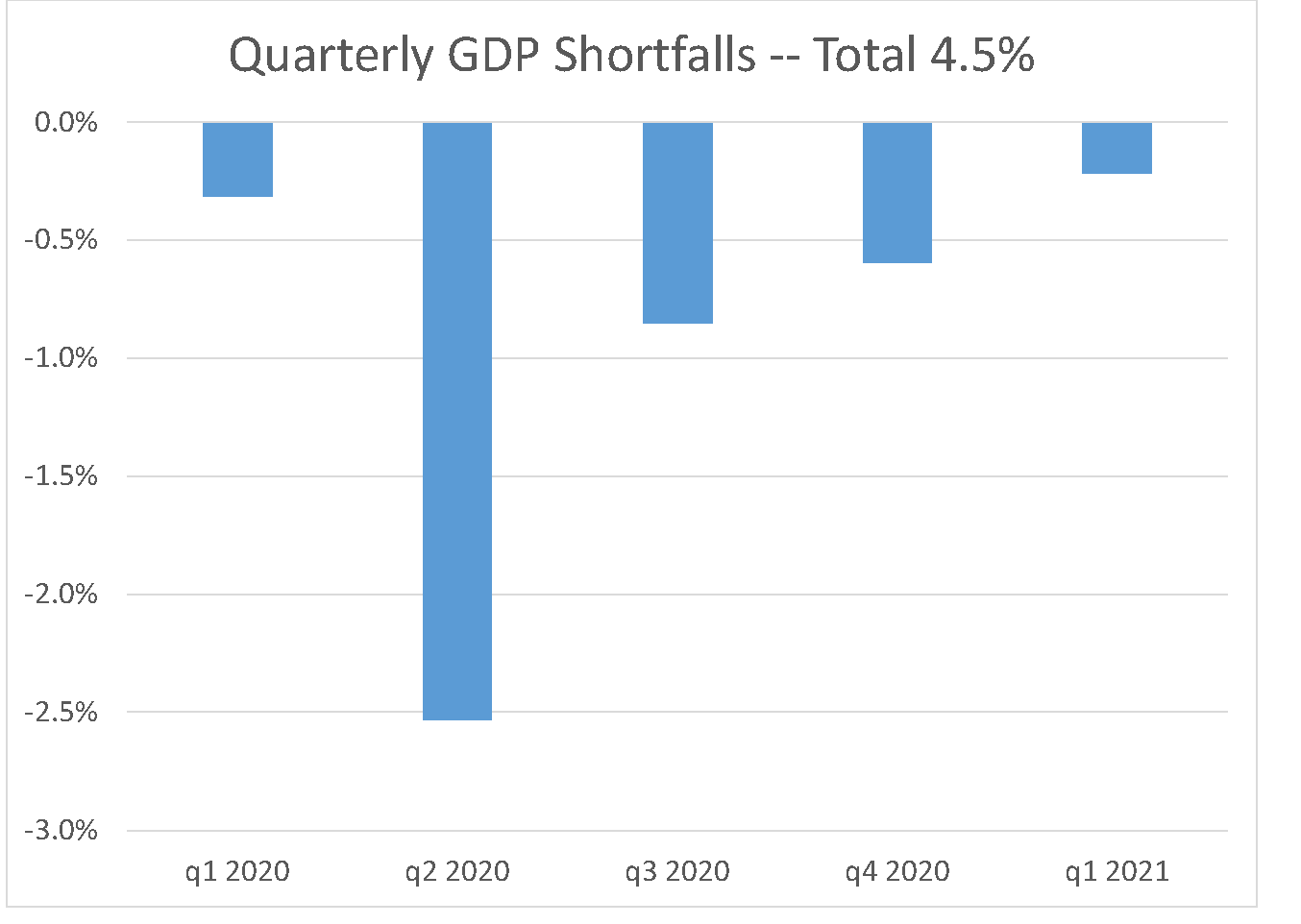

That quarterly peak was obliterated in the second quarter of 2020, when the lost production was equal to 2.5% of a full year’s output. Altogether, the shortfalls in the five quarters were equal to 4.5% of peak GDP.

[1] A more precise approach, in theory, would be to compare output, amid the recession and recovery periods, to a measure of potential real GDP. As we have noted elsewhere, potential GDP estimates are fraught. Moreover, in a number of cases, the economy operated below estimates of potential GDP for quite a few years after the recession ended. Cumulative theoretical shortfalls, in such circumstances, likely reflect dynamics outside of the effects of recession.

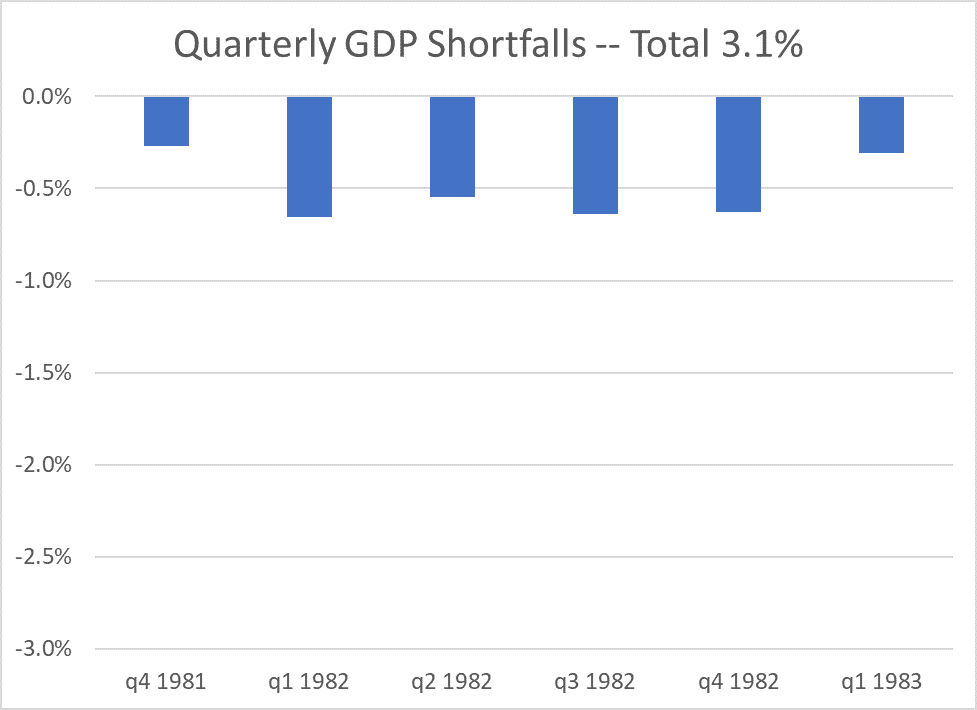

The only other postwar cycle that produced total shortfalls of more than 3% of GDP was the 1981-’83 one, where the total was 3.1%. Downturns that began in 1953, 1957 and 1973 were the others that cost more than 2% of total output. So, in terms of foregone national GDP, this recession was worse than any but one in the past 70 years – even if it was the shortest. So, in terms of foregone national GDP, this recession was worse than any but one in the past 70 years – even if it was the shortest.

One big caveat. Each July the Bureau of Economic Analysis provides benchmark revisions to its estimates for real GDP. On July 29th we will get this year’s adjustments. We must warn that in years exhibiting wild volatility, revisions tend to be wild as well. . .