Over the last 12 months, inflation has increased 5.4 percent in the US. Stoked by a leap for energy prices and a hefty 4.3 percent rise for core inflation. Throughout most of U.S. post-war history core goods price increases, on average rose at a much slower pace than services prices. Not so over the past 12-months. Strikingly, the July year-on-year gain for core goods prices, 8.5 percent, towers over the 2.9 percent increase in core services prices. Since the history of muted core goods price increases owe much to cheaper imported goods from Asian emerging economy nations, it is natural to wonder if Asia is now, in contrast, exporting big price increases to the U.S.

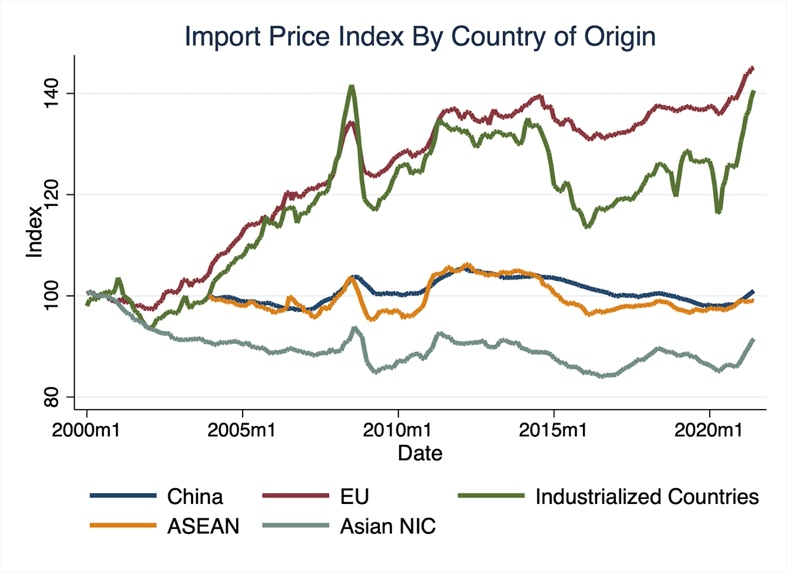

As the chart below powerfully demonstrates, Asian nation exports to the U.S. have carried flat to falling price tags, compared to the modestly rising prices from the EU and more generally from all Industrialized Countries

(Import/Export Price Indexes (MXP)).

Has the pandemic changed this narrative? Using the same dataset, and looking at the past two years, it is clear that Asian import prices have risen over the period. Again, however, their rise stops well short of the increases registered by Industrialized nations.

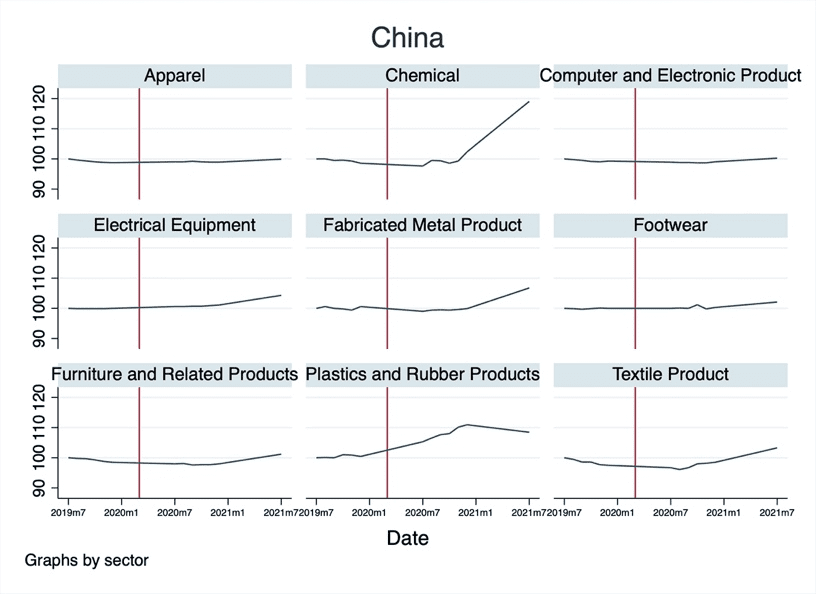

To better understand the drivers of aggregate import price indexes, we use the sectoral indexes (normalized to July 2019 levels). First, we look at the import prices from the major trade partner China. Import prices have been increasing in the Chemical and Plastics and Rubber sectors. However, the prices for the goods that matter most (the highest trade share) in US imports from China, such as Apparel, Computer and Electronics, Furniture and Textiles, have been stable since the beginning of the pandemic.

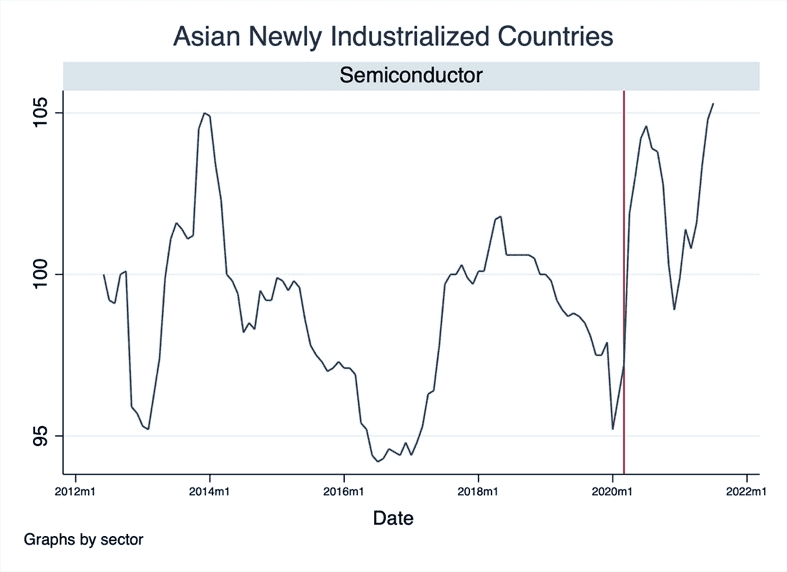

Another angle of the discussion has been around the supply side disruptions and global Semiconductor shortages. Increasing used car prices in the US have further sparked the debate. Here, we only look at the Semiconductor and Electronic import price index (available since June 2012) from Asian Newly Industrialized Countries. We present the prices for the entire sample rather than focusing on the recent period to show how fluctuating this price index in general is. Semiconductor import prices have clearly surged since March 2020. But this is a highly volatile price series, and we believe that it is too soon to say there exists anything unusual.

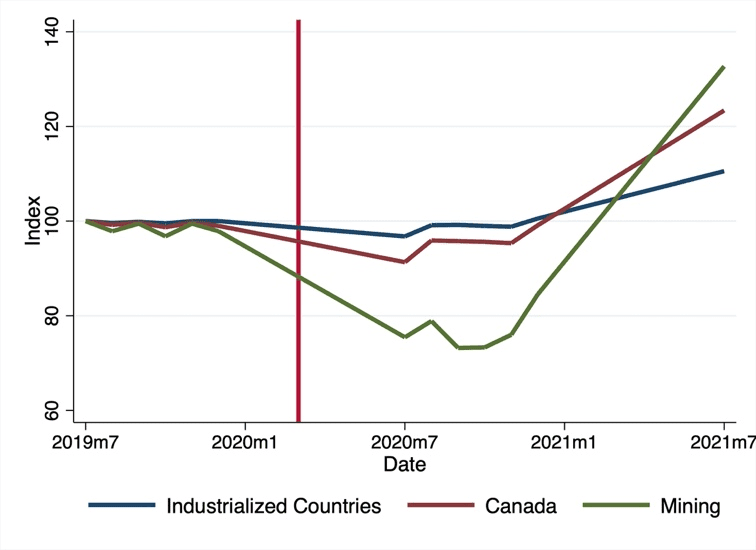

Clearly, amid the pandemic the US has been experiencing its biggest price pressures from Industrialized Countries. This jump, however, is greatly influenced by the sharp increase in import prices from Canada. Furthermore, the mining import prices have been the reason behind the trend in Canadian import prices.

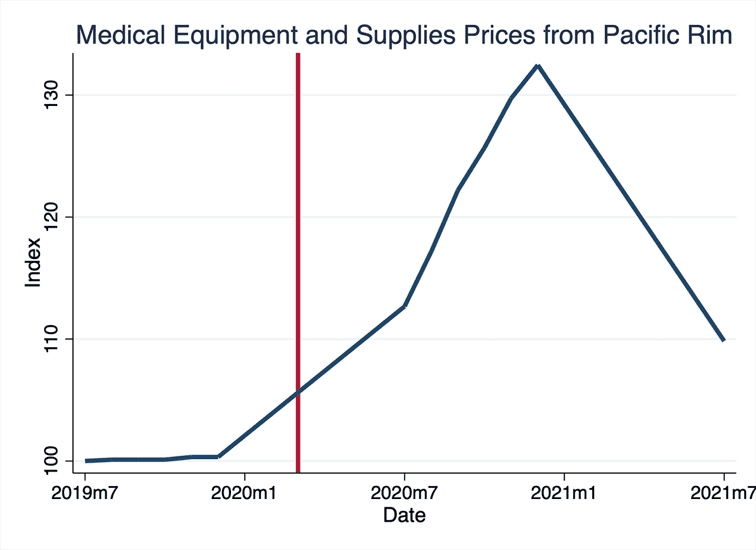

Lastly, we would be remiss if we failed to offer up a clear snapshot of supply and demand dynamics during the pandemic. The last figure shows how stable the medical equipment and supplies import prices (from Pacific Rim) were before the pandemic and how prices skyrocketed right after the pandemic. It is a simple example of how excess demand can generate a—so far temporary—surge in prices.