Herbert Stein, former Chair of the U.S. Council of Economic Advisors for R.M. Nixon, reminded his colleagues that “if something cannot go on forever, it will stop”. History is littered with speculators who went broke, betting against clearly unsustainable trends but forgetting that forever is a long time.

Which brings us to the Chinese Real Estate boom of the past 20 years. By almost any metric imaginable, China’s investment in residential real estate has gone from excessive to inconceivable.

But China is, when it wants to be, a command-based economy. And commitment to strong growth, time and again, led Chinese provinces to support ever more expansive housing construction, resulting in a rise of direct real estate investment from 5% to 15% of real GDP, with related sectors suggesting real estate gains influenced close to 30% of GDP. This unfolded amid paradoxically simultaneous surges in both housing prices and vacancy rates.

Until now. Evergrande Real Estate’s financial woes and the collapse of aptly named Fantasia Real Estate, has been met by government comments that suggest safety nets of some sort will appear for swindled home buyers and duped individual investors. But no one, it appears, will throw a life line to developers. It looks like President Xi has judged that, for the real estate boom of the past 20 years, forever has arrived and the real estate boom is going to stop NOW.

One first official hint? Real GDP gains, year over year, as of 2021:Q3 fell below 5%, with the construction component of real GDP falling and with quarter-to-quarter real GDP going sideways. Increasingly, official talk is gearing forecasters to expect more weakness to come.

JHU has some data that corroborates the need for this to happen. We published an alternative measure of China’s economic performance, based upon our analysis of satellite captured light intensity, emanating from Chinese cities. In a recently published paper the details describing this analysis is provided.

In a CFE post, May 2019, we provided some summary discussion of the work:

In December of last year, we introduced a new measure for China’s real income gains. The unique aspect of our effort reflects our statistical analyses of satellite imaging of nighttime Chinese city lighting. As we noted in our previous essay, analyses of the growth for nighttime city illumination, correctly filtered, closely mirrors the climb for national output for a whole host of countries. China, however, is a glaring exception. Gains for city lights have been systematically weaker than official estimates of Chinese real GDP growth, and this divergence has worsened over the past two years.

A naive interpretation of our data would lead one to assert that China’s claims about real gross domestic product gains are greatly inflated. We have a more nuanced view. Other critics of official data have done bottom-up analyses and conclude that China’s real GDP data greatly overstates the level of investment activity—the booming sector driving China’s growth over the past decade—a reflection of regional officials’ exaggerating the gains for construction, in an effort to claim that they have met overall growth targets.

We don’t doubt that some officials provide fanciful claims about investment rates. We conjecture, however, that a significant additional part of the mismatch between our illumination data and the official GDP tally reflects the increasingly uneconomic nature of Chinese investments in office and residential real estate. Despite soaring vacancy rates, investment continues to rise. Increasingly, however, the buildings go up, but the lights don’t go on.

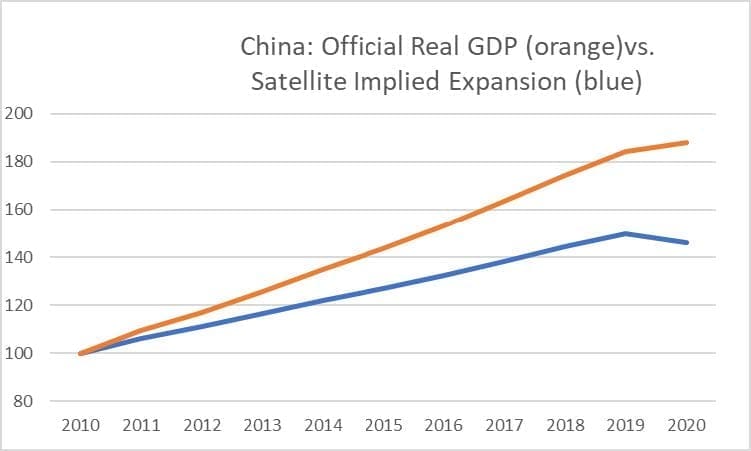

Last week we updated our analysis, capturing 2020 satellite suggested gains for the Chinese economy versus the official tally. Our results were eye opening. According to our data citywide illumination, in 2020, actually contracted by 2.5%.

The chart above (Figure 1) represents official tallies of Chinese real GDP, versus our inferred gains for productive output, based upon growing illumination in Chinese cities. Two things are true. Official data consistently exceeded satellite readings, with the 2010-2019 growth rate of 7%, well in excess of the 4.9% satellite linked rate. In addition, in 2020, modest official growth is completely at odds with an outright decline we compute for 2020 citywide illumination. As we see the data, in 2020, housing units continued to go up, but nearly none of the building’s lights went on.

The absence of night light gain, in the midst of a prodigious 2020 construction boom, we would suggest, makes perfect sense in a nation with unprecedented house prices and sky-high vacancy rates. Home buyers in the major metropolitan areas, were neither first time buyers nor soon to be renters. China real estate home price gains apparently reflected confidence in one thing. More gains for home prices.

Bitcoin has gone to astronomical levels, as its advance has forced ever more inclusive groups into the game. Bitcoin, however, has an advantage over housing in China. It has no valuation metric. China real estate, in stark contrast, now sport prices that are wild. They are wild relative to median household incomes. They are wild versus potential rental incomes. They total to a real estate sector valuation that is wild relative to the size of the Chinese economy. And in the major Chinese metropolitan area, they dwarf valuation measures for both London and New York. Indeed, on almost all of these metrics, current values are, as Vizzini utters in The Princess Bride, “Inconceivable.”

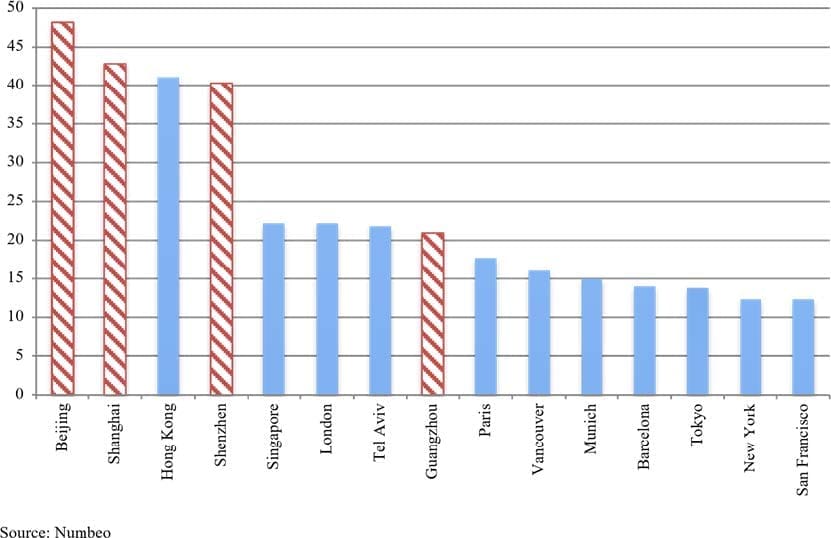

We believe our satellite imaging work complements another recent paper. Ken Rogoff and Yuanchen Yang, in a paper published in 2020, round up a great many of the improbable valuations that now exist in the Chinese real estate universe.

Our two favorites? Despite China and the U.S. having comparable sized economies, China’s real estate market is now worth more than twice the U.S. market. Second, in the elite real estate markets in China, the median house price is more than 40 times the median household disposable income. We reproduce the Rogoff/Yang chart below:

All of which leads us embrace Herb Stein’s dictum and to suggest that it looks to us like real estate investment growth will stop NOW.

How might this play out in China? Most agree that China’s unflinching willingness to bail out before sheer hell breaks out, limits the financial contagion Lehman crisis effects witnessed in the U.S. in 2008-2009. But real economy effects are another matter.

China’s real estate boom has accounted for much of the overall economies advance over the past decade. And real estate construction accounted for 29% of GDP in 2019 (Rogoff/Yang). Given the extraordinary overhang of unlit housing stock, one has to expect that the bust for this boom will involve large outright declines for real estate investment flows, not slowing growth rates. Importantly, as we see it, contracting city nighttime illumination begs policymakers to pull the plug on increasingly useless construction and the Rogoff/Yang collection of inconceivable excesses reinforce the point.

Let’s play with some numbers. Suppose real estate falls by 15% per year, in 2022 and 2023. Suppose further, thanks to widespread efforts to catalyze growth elsewhere, the rest of the economy grows at 6% per year. In such circumstances, as 2023 comes to a close, real estate will still amount to over 20% of the economy, and the overall economy will have registered two years of next to no growth.

We would bet that President Xi sends consumers some form of lifeline. We can also conjecture that, beyond that, China will likely try and replace real estate boom with broad based construction expansion elsewhere, perhaps in renewables energy construction.

But for a time, if China has now decided that they must end the business of pouring concrete, bending steel, and fitting glass windows for edifices whose lights don’t go on, their demand for raw materials, will likely contract sharply. In a world that currently embraces the notion that all systems point to higher inflation, China’s real estate bust could turn out to have surprising consequences that extend well beyond its shores.